When Cost is THE Conversation: What You Need to Know for 2026 Health Insurance Outreach

Marketing for Change has conducted consumer research for federal and state health insurance enrollment projects for two decades. Our findings have consistently reinforced one essential rule: cost matters most, no matter what.

But this year, our data is showing an important shift in the enrollment landscape. In 2026, cost isn’t just leading the conversation. It is the conversation. A combination of expiring enhanced subsidies, rising premiums, and broader economic pressure has fundamentally changed how consumers of all income groups are evaluating health coverage.

The differences for 2026 are most stark among the estimated 27 million Americans who don’t have health insurance. This group nearly universally wants health insurance. But they are quick to decide that they simply can’t afford it and, once they do, all other communications are quickly tuned out.

Assessing the Landscape

To better understand the dynamics of the 2026 enrollment landscape, Marketing for Change conducted a national online survey early this year, right after the close of the most recent Marketplace open enrollment period. The goal was to:

- Explore how different insurance coverage groups – including uninsured, self-insured, Marketplace-insured, and group-insured (employer, etc.) – are thinking about health insurance right now;

- Understand what is driving decision-making;

- Measure their knowledge, beliefs, and attitudes about health insurance; and

- Understand their immediate and future health insurance plans.

Affordability concerns are not just elevated, they dominate consumer decision-making at an even higher level than they have in previous years.

Across audiences, one theme stood out: affordability concerns are not just elevated, they dominate consumer decision-making at an even higher level than they have in previous years.

Rising Costs Are Reshaping Perceptions

Data from the most recent national Open Enrollment period is a case in point. Residents in 28 states use the Federally Facilitated Marketplace to choose insurance plans offered under the Affordable Care Act. These plans include four levels of coverage: Bronze, Silver, Gold and Platinum, with each level up providing more comprehensive coverage, usually at a higher cost.

This past enrollment period, the average monthly premium for Silver plans increased by an average of 31%. Bronze plans also saw increases of around 16%. As a result of these increases, an average Bronze plan in 2026 (around $658) cost more than an average Silver plan in 2025 (around $628).

These aren’t modest changes. They’re the kind that consumers notice immediately, and the behavioral impact is already visible. Marketplace enrollees appear to be trading down, shifting from more generous Silver options to lower-cost – and lower coverage – Bronze alternatives.

These shifts also impact how insured individuals view the entire health insurance industry. Our survey shows that individuals whose premiums increased report significantly more negative attitudes toward health insurance overall.

Those who experienced significant premium increases were more likely to believe that “health insurance companies do not care about people like me” or “all health insurance is a scam.” When the price goes up, trust in the health insurance system is impacted.

Cost Isn’t Just One Factor, It’s the Doorway

When we asked consumers to identify the single most important feature of a health insurance plan, the results were striking. Low monthly premiums dominated (by a magnitude of 4 to 5 times) across every insurance group, but especially among the uninsured, where nearly two-thirds ranked it as their top priority. No other feature — deductibles, provider networks, or covered services — came close. This is potentially not surprising, as cost is always a top concern. But this year price dominates other features of health insurance at a much higher rate than even the past few years, and the gap between cost concerns and other health insurance decision points has dramatically expanded.

This isn’t just a preference. Cost is the doorway into even considering purchasing health insurance. Before consumers consider networks, benefits, or even access to care, they’re asking a more basic question: Can I afford this at all? If the answer feels like “no,” the rest of the conversation never happens.

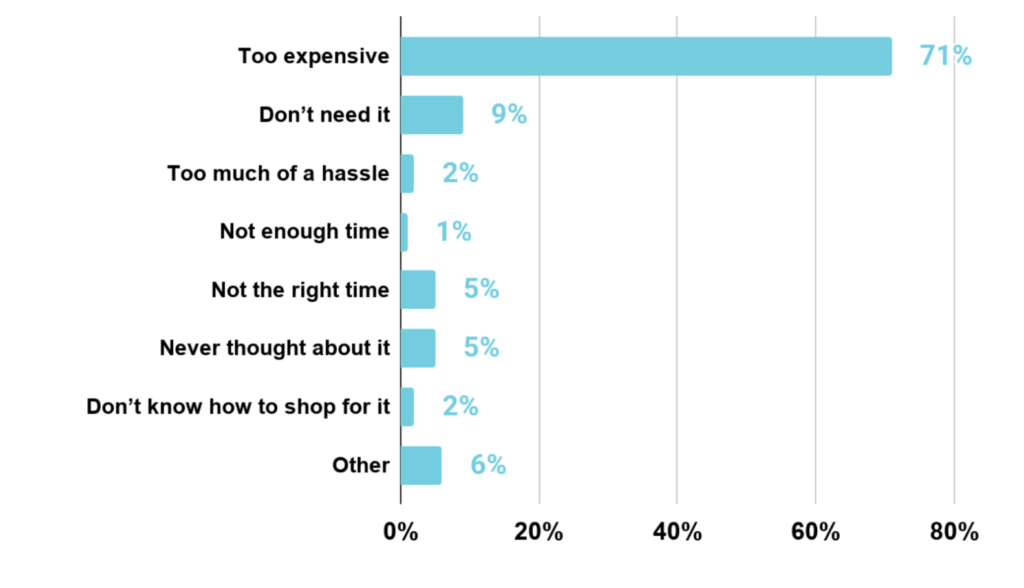

That dynamic is even clearer when looking specifically at uninsured individuals.

Uninsured: Why didn’t you consider getting health insurance?*

Cost isn’t just a top concern. It’s the primary reason many uninsured never seriously considered enrolling in coverage to begin with.

This matters because it challenges a common assumption in outreach: that the uninsured are simply unaware of insurance options, disengaged, or hard to reach. In fact, many are actively making difficult decisions based on cost.

It’s easy to interpret these findings as purely economic. Premiums go up, so enrollment interest goes down. But it’s important to remember that cost concerns are deeply tied to uncertainty and lead to questions like: Will I actually use this coverage? Is this worth it compared to everything else I need to pay for? In a moment of broader financial strain, those questions carry more weight, and they make consumers more cautious, more skeptical, and less responsive to traditional messaging.

Breaking through the cost barrier

Importantly, the data also suggests that cost barriers should not be mistaken for lack of interest.

Among uninsured individuals in our survey who either did not consider coverage because of cost or ultimately chose not to purchase it because of affordability concerns, 92% said they would prefer to have health insurance. Only 7% said they do not ever want coverage.

Most uninsured consumers are not rejecting the idea of health insurance, they are struggling with whether it feels financially attainable.

That distinction matters for outreach efforts. Most uninsured consumers are not rejecting the idea of health insurance, they are struggling with whether it feels financially attainable.

In the coming year, reaching uninsured Americans will require more than awareness campaigns alone. Outreach and messaging must recognize the economic realities consumers are facing, clearly communicate affordability, and reinforce that coverage can still provide meaningful financial protection in an increasingly uncertain environment.

In future posts, we will highlight additional data from our survey that hints at potential openings and strategies to break through the cost barrier.

Aaron Metzger leads the agency’s consumer research for the federal Health Insurance Marketplace as well as for state exchanges in Illinois and Nevada.

Aaron Metzger is the director of research at Marketing for Change.

Sign Up

Get insights to help your cause delivered directly to your inbox once a month.